GUIDANCE ON 2025 PIT FINALIZATION

HƯỚNG DẪN QUYẾT TOÁN THUẾ THU NHẬP CÁ NHÂN NĂM 2025

Income included in PIT Finalization / Thu nhập kê khai quyết toán thuế TNCN

VSOL declares and finalizes PIT based on the actual income payment date, in compliance with the prevailing PIT regulations.

Accordingly, income arising from the December 2025 payroll (including December 2025 salary and the 13th-month salary) is paid on January 5, 2026, and therefore will be declared and finalized in tax year 2026.

As a result, the PIT finalization for tax year 2025 only includes income paid during 2025, corresponding to 11 payroll periods, from January 2025 to November 2025.

VSOL thực hiện kê khai và quyết toán thuế TNCN theo thời điểm chi trả thu nhập, phù hợp với quy định của pháp luật thuế TNCN hiện hành.

Theo đó, thu nhập phát sinh từ kỳ lương tháng 12/2025 (bao gồm lương tháng 12/2025 và tiền lương tháng 13) được chi trả vào ngày 05/01/2026, nên sẽ được kê khai và quyết toán vào kỳ thuế năm 2026.

Vì vậy, quyết toán thuế TNCN năm 2025 chỉ bao gồm thu nhập được chi trả trong năm 2025, tương ứng với 11 kỳ lương, từ kỳ lương tháng 01/2025 đến kỳ lương tháng 11/2025.

Authorization for Company to conduct PIT Finalization on your behalf / Trường hợp ỦY QUYỀN cho công ty quyết toán thay

You may authorize the Company to finalize PIT for you for tax year 2025 if you fall into one of the following two cases:

1. In 2025, you have only income from salary/wages under a labor contract of 3 months or more, solely at VSOL;

OR

2. In 2025, you have only income from salary/wages under a labor contract of 3 months or more, solely at VSOL, and additional incidental income from other sources that meets all three conditions below:

- Average income does not exceed VND 10 million per month (equivalent to VND 120 million per year); and

- PIT has been withheld at a flat rate of 10% by the paying entity; and

- You do not wish to finalize PIT for this incidental income.

Nhân viên có thể ủy quyền cho công ty quyết toán thuế TNCN năm 2025 thay bản thân nếu thuộc một trong hai trường hợp sau:

1. Năm 2025, chỉ có thu nhập từ tiền lương, tiền công với HĐLĐ từ 3 tháng trở lên DUY NHẤT tại VSOL;

HOẶC

2. Năm 2025, chỉ có thu nhập từ tiền lương, tiền công với HĐLĐ từ 3 tháng trở lên DUY NHẤT tại VSOL, đồng thời CÓ THÊM THU NHẬP VÃNG LAI ở nơi khác đáp ứng đủ 3 ĐIỀU KIỆN:

- Bình quân không quá 10 triệu đồng/tháng (tương đương 120 triệu đồng/năm), và

- Đã khấu trừ thuế TNCN đủ 10% tại đơn vị chi trả thu nhập và

- Không có nhu cầu quyết toán thuế cho phần thu nhập vãng lai này.

Authorization Procedure / Hướng dẫn thực hiện ủy quyền

Timeline Thời gian |

|

Submission of Authorization Letter Nộp giấy ủy quyền |

|

In case of tax refund or additional tax payable Trường hợp phát sinh hoàn thuế hoặc nghĩa vụ thuế TNCN phải nộp thêm |

|

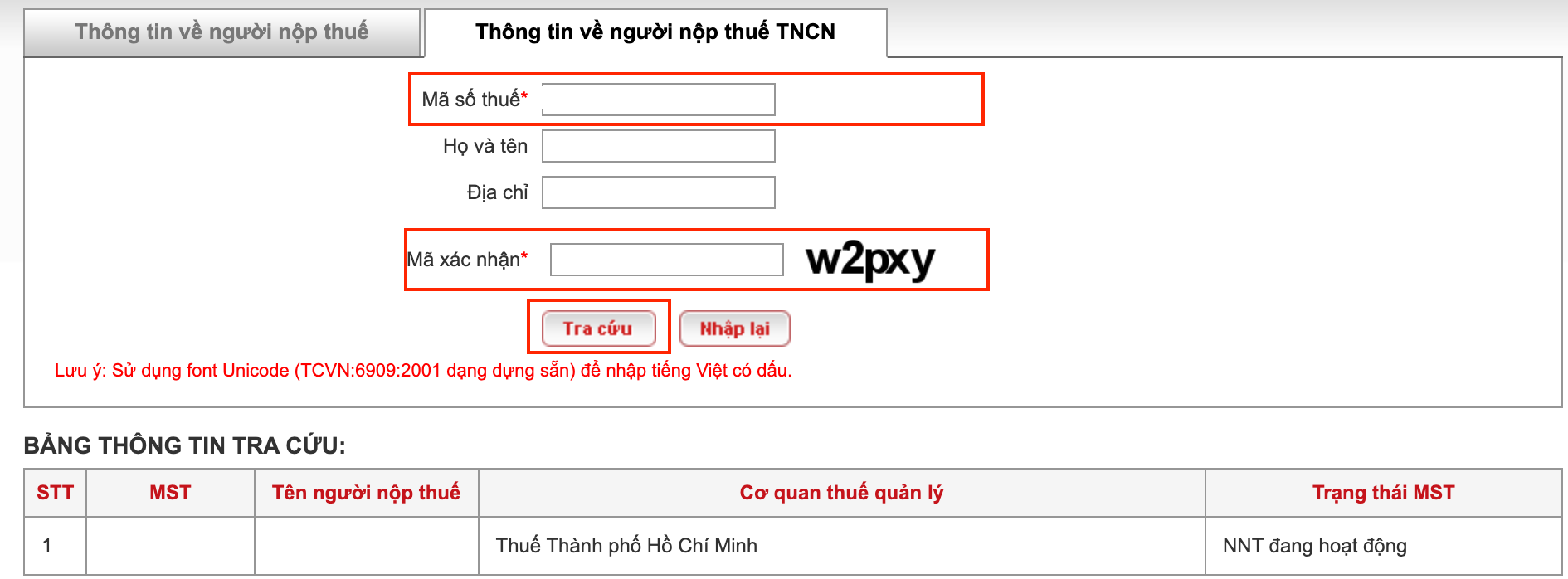

Guidance on checking your Personal Tax Code / Hướng dẫn tra cứu mã số thuế

Access the website https://tracuunnt.gdt.gov.vn/tcnnt/mstcn.jsp, at the section “Personal Income Taxpayer Information”, enter your 12-digit Citizen ID Number, input the verification code, and select “Search” to retrieve your Tax Code.

Truy cập website https://tracuunnt.gdt.gov.vn/tcnnt/mstcn.jsp, tại mục Thông tin về người nộp thuế thu nhập cá nhân, nhập số CCCD 12 số của bản thân + mã xác nhận và chọn Tra cứu để có thông tin về mã số thuế

Self-Finalization of PIT / Trường hợp TỰ QUYẾT TOÁN

If you do not fall under either case stated in section "Authorization for Company to conduct PIT Finalization on your behalf", you are required to self-finalize your PIT, with the following notes:

Nếu không thuộc một trong hai trường hợp nêu tại mục "Trường hợp ủy quyền công ty quyết toán thay", nhân viên cần tự thực hiện việc quyết toán thuế với lưu ý như sau

Timeline for Providing PIT Withholding Certificates Thời gian cung cấp chứng từ khấu trừ thuế TNCN |

|

For employees still working at the time of issuance Với nhân viên còn làm việc tại thời điểm công ty cung cấp chứng từ |

|

For employees no longer working at the time of issuance Với nhân viên không còn làm việc tại thời điểm công ty cung cấp chứng từ |

|

Finalization Cases and Deadlines Trường hợp và thời hạn thực hiện quyết toán |

|

Full Income Declaration Kê khai đầy đủ thu nhập |

|

Notes / Lưu ý

FAQ / Các câu hỏi thường gặp

Question Câu hỏi | Answer Câu trả lời |

Can an individual who terminates their labor contract with VSOL effective March 26, 2026 authorize VSOL to finalize personal income tax on their behalf? Cá nhân chấm dứt HĐLĐ tại VSOL từ ngày 26/03/2026 thì có được ủy quyền cho VSOL quyết toán thuế thay không? | Not eligible to authorize VSOL to finalize Personal Income Tax (PIT) for tax year 2025. Reason: Under current regulations, an individual may only authorize an employer to perform PIT finalization if they are still employed by the company at the time the company carries out the tax finalization. The company’s deadline for PIT finalization for tax year 2025 is March 31, 2026. Không được ủy quyền cho VSOL quyết toán thuế TNCN năm 2025. Lý do: Theo quy định, cá nhân chỉ được ủy quyền quyết toán thuế cho doanh nghiệp khi đang làm việc tại doanh nghiệp tại thời điểm doanh nghiệp thực hiện quyết toán thuế (thời hạn quyết toán thuế năm 2025 của doanh nghiệp là ngày 31/03/2026). |

Trong năm 2025, cá nhân ký Hợp đồng lao động (HĐLĐ) từ 3 tháng trở lên và phát sinh thu nhập từ 02 công ty trở lên thì có được ủy quyền cho VSOL quyết toán thuế thay không? | Không được ủy quyền cho VSOL quyết toán thuế TNCN năm 2025. Lý do: Trường hợp trong năm 2025 cá nhân có thu nhập phát sinh tại từ 02 công ty trở lên, và các khoản thu nhập này đều phát sinh từ hợp đồng lao động từ 03 tháng trở lên, thì cá nhân bắt buộc phải trực tiếp thực hiện quyết toán thuế TNCN với cơ quan thuế. |

If, in 2025, an individual signs a labor contract with a term of three (3) months or more and earns income from two or more companies, can they authorize VSOL to finalize personal income tax on their behalf? Ngoài thu nhập từ HĐLĐ từ 3 tháng trở lên tại VSOL, nếu trong năm 2025 cá nhân còn có thu nhập ở nơi khác thì có được ủy quyền cho VSOL quyết toán thuế thay không? | Authorization eligibility is determined based on the nature of income earned outside VSOL, specifically as follows:

→ Not eligible for authorization. The individual is required to self-finalize personal income tax (PIT).

→ Eligible for authorization, provided that all three (3) conditions below are met simultaneously:

→ If any of the above conditions are not met, the individual is required to self-finalize PIT with the tax authority. Việc ủy quyền được xác định căn cứ vào bản chất của khoản thu nhập phát sinh ngoài VSOL, cụ thể:

→ Không được ủy quyền, cá nhân phải tự quyết toán thuế.

→ Được ủy quyền nếu đồng thời đáp ứng cả 3 điều kiện sau:

→Trường hợp không đáp ứng một trong các điều kiện trên, cá nhân phải tự thực hiện quyết toán thuế TNCN với cơ quan thuế. |

If an individual joins VSOL during 2025 (i.e. does not work for the full 12 months), are they eligible to authorize the Company to finalize personal income tax on their behalf? Cá nhân gia nhập VSOL trong năm 2025 (không làm việc đủ 12 tháng) thì có được ủy quyền cho công ty quyết toán thuế thay không? | An individual who works for less than 12 months may still authorize VSOL to finalize Personal Income Tax (PIT) if they fall into one of the following two cases:

OR

Cá nhân làm việc dưới 12 tháng vẫn có thể ủy quyền cho VSOL quyết toán thuế TNCN nếu thuộc 1 trong 2 trường hợp sau:

HOẶC

|

If an individual signs a labor contract solely with VSOL starting from January 2025, but their December 2024 salary under the labor contract was paid by the former employer in January 2025, are they eligible to authorize VSOL to finalize personal income tax on their behalf? Cá nhân ký HĐLĐ duy nhất với VSOL từ tháng 01/2025, nhưng tiền lương tháng 12/2024 theo HĐLĐ được công ty cũ chi trả vào tháng 01/2025 thì có được ủy quyền cho VSOL quyết toán thuế thay không? | This case should be determined based on the tax year in which the December 2024 salary paid by the former employer is declared. The individual should contact the former employer to confirm this information.

→ In 2025, the individual is considered to have income only from VSOL. → Eligible to authorize VSOL to perform PIT finalization on their behalf.

→ In 2025, the individual is considered to have income from two or more entities. → Not eligible for authorization; the individual must self-finalize PIT. Trường hợp này cần căn cứ vào năm kê khai thuế của khoản lương tháng 12/2024 tại công ty cũ. Cá nhân cần liên hệ công ty cũ để xác nhận thông tin.

→ Năm 2025 được xác định là chỉ phát sinh thu nhập tại VSOL → Được ủy quyền cho VSOL quyết toán thuế thay.

→ Năm 2025 cá nhân có thu nhập tại từ 02 đơn vị trở lên → Không được ủy quyền, cá nhân phải tự quyết toán thuế. |

In 2025, if an individual works at a former company as an intern and later signs an official labor contract with VSOL, are they eligible to authorize VSOL to finalize personal income tax (PIT) on their behalf? Năm 2025, cá nhân làm việc tại công ty cũ với tư cách Intern, sau đó ký hợp đồng lao động chính thức tại VSOL thì có được ủy quyền cho VSOL quyết toán thuế TNCN thay không? | An individual may authorize VSOL to finalize Personal Income Tax (PIT) on their behalf only if all of the following conditions are met simultaneously:

If any of the above conditions are not met, the individual is required to self-finalize PIT with the tax authority. Cá nhân được ủy quyền cho VSOL quyết toán thuế TNCN thay nếu đồng thời đáp ứng đầy đủ các điều kiện sau:

Trường hợp không đáp ứng một trong các điều kiện trên, cá nhân phải tự thực hiện quyết toán thuế TNCN với cơ quan thuế. |

In 2025, if an individual earns income only from an internship at VSOL during the period from October to December 2025, and only signs an official labor contract with VSOL in January 2026, are they eligible to authorize VSOL to finalize personal income tax (PIT) for tax year 2025 on their behalf? Trong năm 2025, cá nhân chỉ phát sinh thu nhập từ công việc Intern tại VSOL trong giai đoạn tháng 10–12/2025. Đến tháng 01/2026 mới ký hợp đồng lao động chính thức với VSOL thì có được ủy quyền cho VSOL quyết toán thuế TNCN năm 2025 thay không? | Not eligible to authorize VSOL to finalize Personal Income Tax (PIT) for tax year 2025. Reason: Authorization for PIT finalization applies only to income arising from labor contracts with a term of three (3) months or more during the relevant tax year. In 2025, the individual’s income arises solely from an internship, and no labor contract has been signed; therefore, the individual does not meet the conditions for authorization and must self-finalize PIT. Không được ủy quyền cho VSOL quyết toán thuế TNCN năm 2025. Lý do: Việc ủy quyền quyết toán thuế chỉ áp dụng đối với thu nhập từ HĐLĐ từ 3 tháng trở lên năm tính thuế. Thu nhập trong năm 2025 đang là thu nhập từ intern và chưa ký HĐLĐ nên không đủ điều kiện để ủy quyền quyết toán thuế. |